Insights on China's new policies, reform initiatives and economic data brought to you from Lead Analyst Jens Presthus

14 April 2023

A slow and uneven recovery prompts spending boom by local governments

Key takeaways

China’s economic recovery is off to a slow start, with households saving even more this year than they did in 2022. The chorus calling for direct household support has therefore grown louder and wider.

Most local officials are, however, turning to the old stimulus playbook – showering manufacturers in subsidies and spending vast sums on transportation infrastructure. This trend is particularly evident in “hinterland” provinces struggling to get any sort of recovery off the ground. Wealthier provinces seem to be doing better.

Non-existent inflation has prompted some to call for more monetary support. But the PBoC is likely to stay quite passive. Monetary easing does not have a good track record for stimulating demand in China, and conditions are already pretty accommodative. Governor Yi Gang will also be concerned about widening interest rate differentials.

The chorus calling for household support is growing louder and wider

In January I suggested that consumption-targeted stimulus would be needed for a sustained post-zero-covid recovery. So far, such stimulus has remained absent, and the recovery has as a result been disappointing.

The chorus in China voicing concern about weak demand and calling for direct household support has therefore grown louder and wider, with policy advisors, academics and economists at most of China’s large brokerages joining in. Cai Fang, Chief Expert at the Chinese Academy of Social Sciences and member of the PBoC’s monetary policy committee, has perhaps gone the furthest – suggesting cash handouts worth 3 trn RMB or 4% of GDP.

While Beijing’s history of fiscal intervention makes such measures unlikely, some policy manoeuvring will likely be needed. This is mainly because the underlying state of the economy is much weaker today compared to 2021, when China emerged from the first round of covid restrictions. Excess savings in 2022 came for instance largely from employment uncertainty and declining income – plus of course a drawdown in paper-wealth due to the real estate downturn. The 2022-savings trend seems to have continued in 2023 as uncertainty lingers, with household deposits in Q1 up 27% from last year’s record number. By contrast, most of the 2020 savings boom was a result of physical barriers to consumption.

With many of the issues weighing on the economy in 2022 still present, now also combined with weakening external demand, it will be much harder to reverse the savings trend and induce new consumption than it was in 2021.

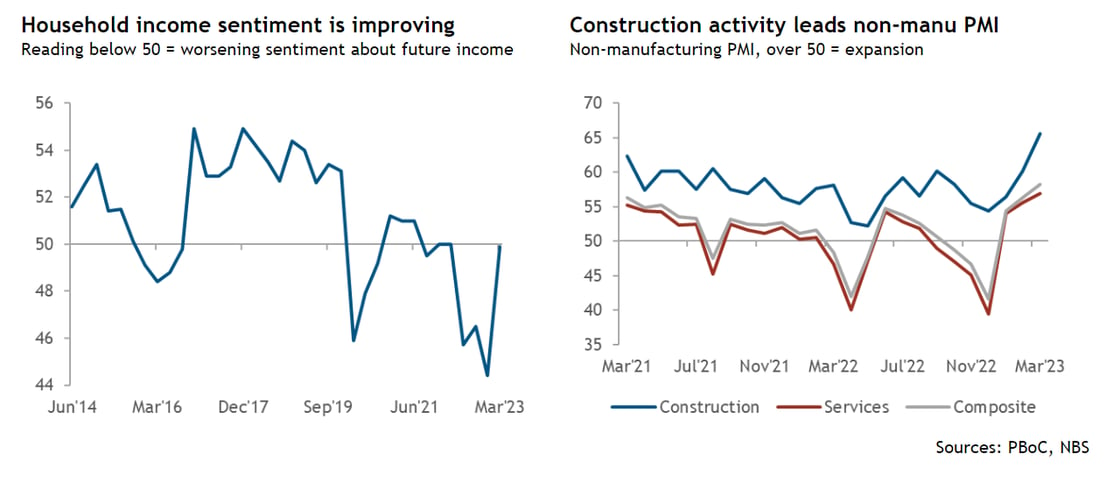

Sentiment indicators show optimism, but hard data points to caution

Various indexes are showing clear signs of improving sentiment. The PBoC’s Urban Depositor Survey for Q1 2023 posted rebounds across all indicators – spanning employment, income and the housing market. PMI readings have also been strong, moving into expansionary territory. There are, however, at least two caveats. The first is that sentiment is improving from a very low level, and any improvement in these indicators should be expected when you exit something like zero covid. Moreover, some indicators remain in negative territory, and the vast majority of households still prefer saving over investing. The second is that the non-manufacturing PMI, which usually is referred to as services PMI, also includes construction activity – which happens to have been the key driver for the non-manufacturing PMI’s strong rebound.

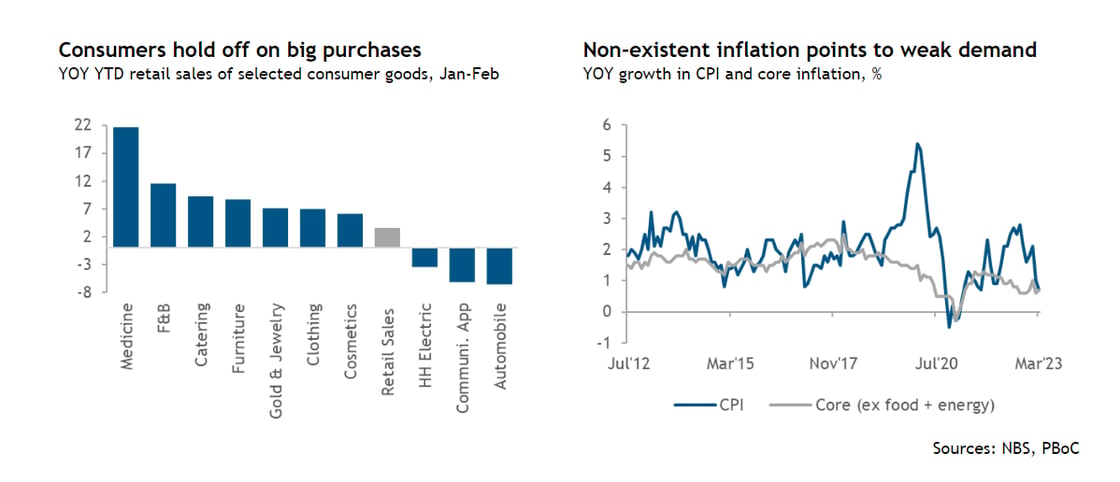

Indeed, the hard data paints a different picture. In addition to the increase in household savings, retail sales have been mediocre, auto sales terrible (after subsidies were withdrawn), imports are declining (even from a low base due to lockdowns at this time last year), unemployment is rising and inflation is more or less non-existent. All of this points to still-weak demand and reluctance among households to start spending again due to remaining uncertainty about the labour market, real estate sector and of course the absence of government support. A recent report by Zhaopin, the online recruiter, noted 47.3% of white-collar workers worry they will lose their jobs this year – up from 39.8% in 2022. This is not something that will help induce more spending.

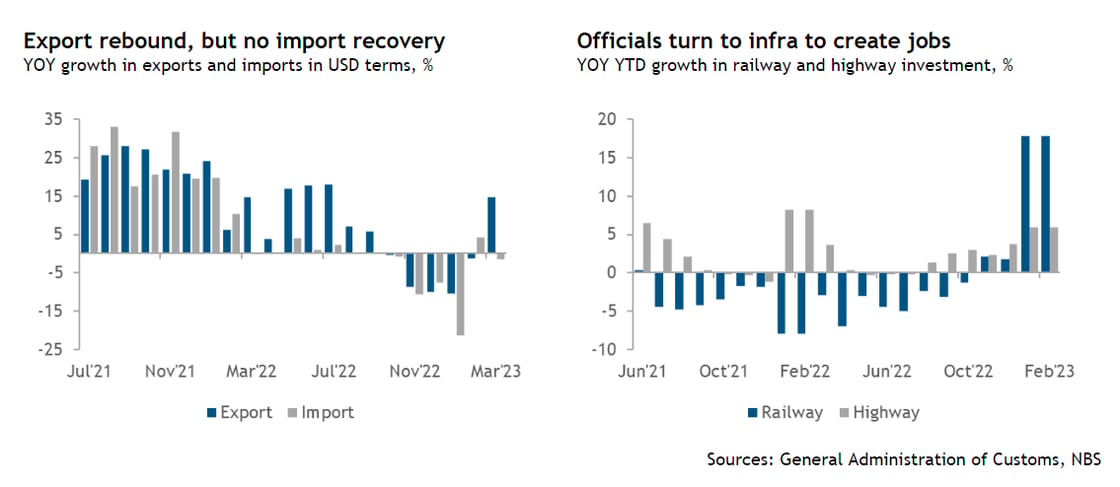

Construction activity has on the other hand been surging. This is not just illustrated in the non-manufacturing PMI reading, but also in loan data which is heavily tilted towards local governments and SOEs who are borrowing for investment in manufacturing (mainly high-tech and energy), digital and transportation infrastructure. Local governments have this year budgeted for a 17% increase in infrastructure spending, which already is showing up in railway investment data. At 113.6 bn RMB for Q1, China is spending more on railways than it has in a decade.

This is worrying not just because China already has all the railway it needs, with these funds being better spent on cash handouts, education and healthcare, but also because additional non-productive investment will add to the already unsustainable debt burdens most local governments are struggling with. Indeed, on April 12th, officials in Guizhou publicly admitted that they would not be able to solve the province’s debt problem without help from Beijing.

The one green shoot ahead of next week’s GDP and retail sales numbers is that household borrowing increased sharply in March – for short-term, medium and long-term loans. This points to renewed optimism about future income prospects and therefore also willingness to spend on consumer goods and real estate. Although of course if debt-based spending is not followed by an increase in income, more of future income will have to be spent on servicing debt. It may also be the case that new loans are taken out to service existing debt, and that the resumption of short-term borrowing is a result of the re-introduction of car and electronics subsidies. Consumption data over the next few months will provide more clarity about this. Finally, it must be noted that data releases over the next few months should be compared to 2019 and 2021 levels in light of the 2020 and 2022 lockdowns.

An uneven recovery, forcing some local officials to turn to old tricks

The economic recovery has also been extremely uneven. Whereas “hinterland” provinces like Henan are struggling with weak demand, poor employment prospects and as a consequence also an inactive real estate sector, “playgrounds for the rich” like Shanghai and Sanya are according to some sources “booming”.

This is in turn impacting how local governments are responding. Henan, for instance, plans to increase infrastructure spending by 50% to 2 trn RMB, while Zhejiang – the wealthy technology and manufacturing hub on the east coast – has budgeted for a 9% cut in infrastructure spending. In other words, provinces that are struggling to instigate a rebound are compensating by spending on things they do not need but which help local officials meet GDP, job creation and other KPIs.

Trade data for March also suggest that local officials continue to shower manufacturers with subsidies to protect jobs and gain additional market share in global trade – two objectives that have been stressed by officials for months, including by Premier Li Qiang during a State Council meeting on April 7th. Indeed, for all the talk about weakening external demand and a 13.6% drop in South Korean exports, China’s March exports rose 14.8% in USD terms – resulting in an $88.2 bn trade surplus – the fifth highest on record. Automobile exports, perhaps unsurprisingly given its strategic focus and weakening domestic demand, almost doubled from March last year to close to 400,000 vehicles.

South Korean and Chinese export data show not only that China is succeeding in its market-share-gaining strategy, but it also underscores that Chinese demand remains weak – given that China is South Korea’s most important export market. Exports to China were down 1/3 in March from 2022.

PBoC to remain on the side-line, with financial conditions already quite accommodative

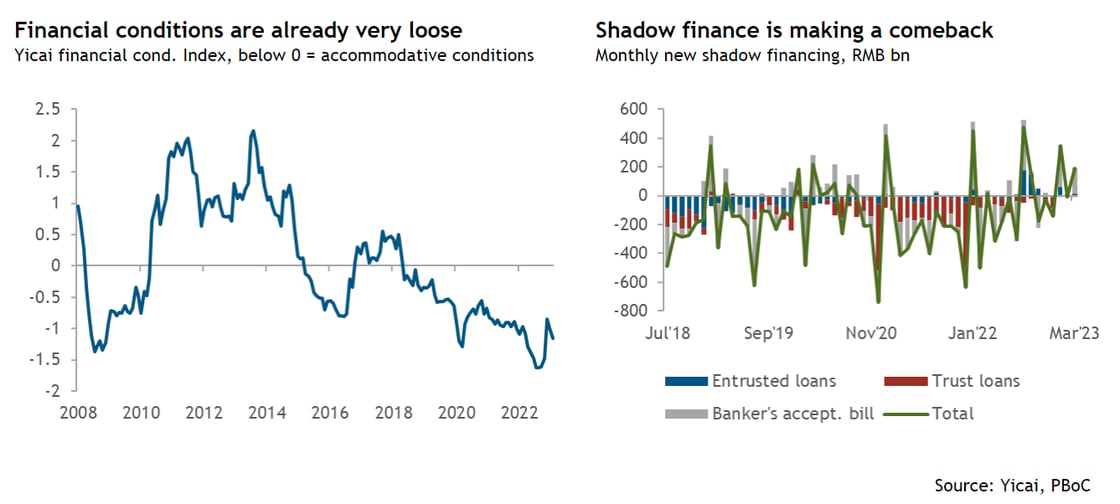

Some easing is possible, but even if demand remains weaker than expected in the coming months, it is unlikely that the PBoC will respond in any meaningful manner. There are at least three reasons for this. The first is that monetary policy is already quite easy. Benchmark rates were lowered two times in 2022 and mortgage rates are at record lows in many cities. Moreover, despite policymakers at the PBoC saying credit growth will be kept stable, at 14.53 trn RMB, aggregate new financing for Q1 was by far the highest on record – representing a 21% increase from the previous high in Q1 2022. Additionally, shadow financing is again increasing after a five-year deleveraging campaign, pointing to relaxed regulatory oversight.

The second reason is that monetary policy historically has not been particularly effective in stimulating demand in China, mainly because most “freed-up credit” by political design tends to flow to businesses and not households.

The third reason has to do with how markets may react to significant monetary easing. Governor Yi Gang will not just be concerned about capital outflows and RMB volatility due to widening rate differentials between China, the US and other developed economies, but also about how a rate cut of size – given how the PBoC has criticised “super easy” monetary policy over the last few years – may be interpreted by markets as the PBoC being very concerned about the state of the Chinese economy. In other words, Governor Yi does not want a repeat of the market reaction that followed the 2015 RMB devaluation.

About Global Counsel

Global Counsel is a strategic advisory business. We help companies and investors across a wide range of sectors anticipate the ways in which politics, regulation and public policymaking create both risk and opportunity – and to develop and implement strategies to meet these challenges. Our team has experience in politics and policymaking in national governments and international institutions backed with deep regional and local knowledge. Our offices in Brussels, London, Singapore, Washington DC, and Doha are supported by a global network of policymakers, businesses and analysts. Find out morehere.