Insights on China's new policies, reform initiatives and economic data brought to you from Lead Analyst Jens Presthus

20 July 2022

China’s ever-widening trade surplus, a bad sign for the economic recovery

Key takeaways

China’s trade surplus widened to almost $100 bn in June, a new record. But this should not be seen as a sign of economic strength. Rather, it is a consequence of domestic demand failing to rebound.

Household confidence surveys by the PBoC and NBS remain stuck at record pessimistic levels. This has led to cautious spending behaviour and a “dash for cash”.

The post-lockdown rebound will therefore be short-lived, similar to after March 2020. This is also bad news for the global economy, as exports to China will continue to fall.

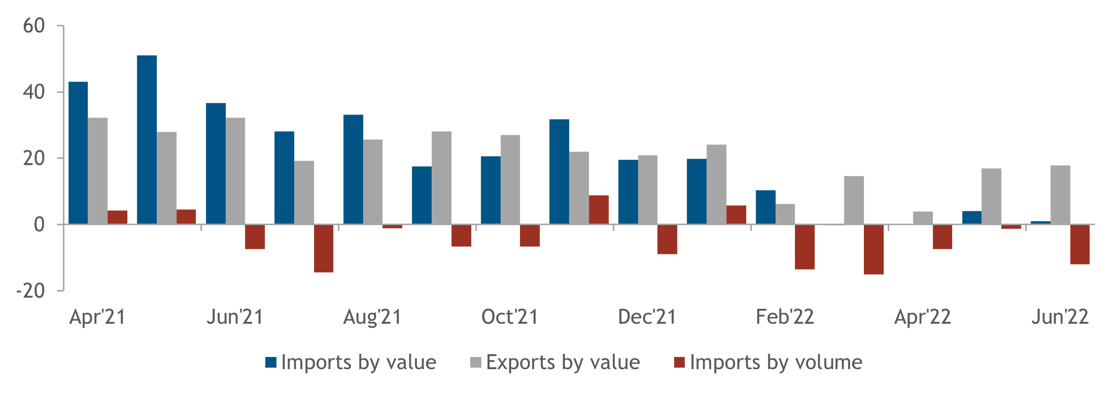

Imports are collapsing as domestic demand stays subdued

Yoy % growth in imports and exports, value in USD and volume in million tonnes

Sources: General Administration of Customs

China’s trade surplus is mostly a domestic demand story

China’s large and ever-growing trade surplus is often pointed to as a testament to its growing economic power, and as a sign that its manufacturing machine in particular is working on all cylinders. June 2022 was no different as China’s trade surplus of $98 bn – a new record – prompted commentary about how the Chinese economy is recovering from covid-related lockdowns. This view, however, is somewhat flawed. While it is true that manufacturing sector activity was strong, with exports growing by 17.9% year-on-year, the record trade surplus is mainly a result of lacklustre domestic demand and a subsequent collapse in imports. At 1% year-on-year growth, the dollar-value of imports grew even slower than in May when Shanghai was still under lockdown. Measured in volume, imports dropped for the fifth consecutive month, down 12% from June 2021. These are not numbers one would expect from an economy that is staging a strong rebound.

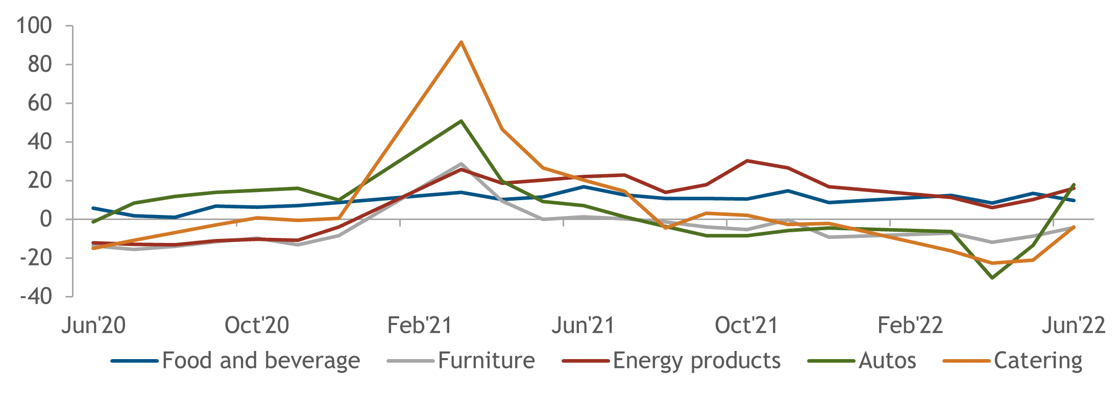

June was always going to see some degree of rebound in household consumption as lockdowns were lifted. However, a close look at retail sales data suggests that a sustained recovery is not on the cards. Besides automobile sales, supported by a government-mandated reduction in car loan interest rates, food and energy were again the main drivers for the 3.9% year-on-year growth in retail sales. Importantly, services continued to lag goods as some covid-19 restrictions were kept in place on restaurants and movie theatres. Catering sales for instance, dropped by 4%, the sixth consecutive month of declines. The Beijing municipal government has since tried to encourage more in-restaurant dining, but targeted vouchers equalling 4.5 yuan per citizen are unlikely to move the needle. Moreover, with the next services sector shutdown just around the corner, as seen in Chengdu on July 18th, it is difficult to build any real momentum in activity.

Strong auto-sales supported retail activity in June, but services continue to lag Provincial finances ex top five revenue generators, RMB trn

Yoy % growth in retail sales of selected goods and services

Source: National Bureau of Statistics

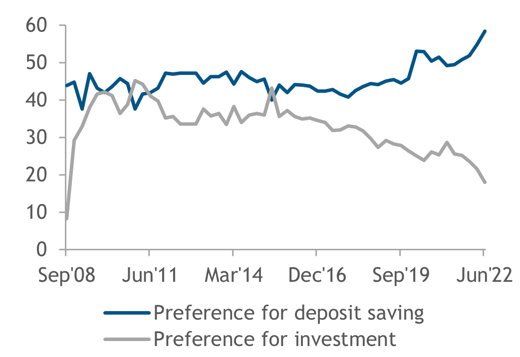

New credit to the household sector has also continued to take the form of short-term loans meant to cover immediate needs and likely increasingly also to service existing debt. New household short-term credit exceeding medium and long-term credit for three months or more in a row has only happened two times over the last 15 years – during the GFC and in 2012 when export reliant Chinese provinces were exposed to both the eurozone crisis and a damaging property market crash.

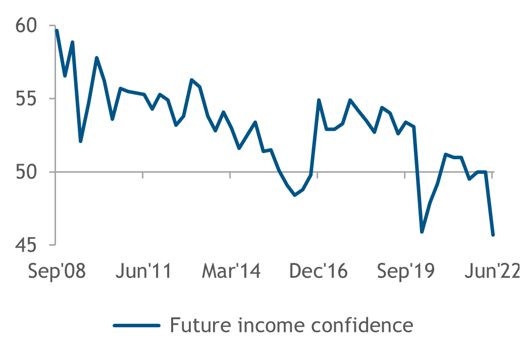

Looking at the People’s Bank of China’s (PBoC) confidence survey for Q2, it seems unlikely that medium and long-term borrowing will pick up in a sustained way anytime soon. In addition to showing that the gap between household preference for saving over investing is widening further, the PBoC’s future income confidence index dropped deep into pessimistic territory at 45.7, even lower than Q1 2020. Furthermore, despite the official urban unemployment rate falling to 5.5% in June – in itself somewhat strange given how 200m flexible workers, or over 25% of the labour force are being impacted daily by zero covid policies – the survey showed that only 10.1% of respondents believe their employment situation will improve over the next few months. This is the lowest reading since the survey started in 2013, and reflects a 19.3% youth unemployment rate – also a record number.

Cash is king for Chinese households…

Savings or investment, % of respondents

…as they expect difficult times ahead

Reading below 50 = worsening sentiment

Source: People’s Bank of China

Where do we go from here?

It has been suggested that moderate inflationary pressures will support China’s economic recovery, because prices for goods and services are not rising as fast as in the US and Europe. But this ignores the point about how low inflation in China is mainly due to excess supply and weak domestic demand, with the opposite having been a driving force for higher inflation in many developed economies since the start of the pandemic. Chinese households have always had the opportunity to consume at moderate price levels, but stagnating wage growth and an uncertain economic outlook is holding them back from doing so.

Importantly, as noted in previous editions of this newsletter, the PBoC is also aware of this. Governor Yi Gang knows that for monetary policy to have any real impact, consumers and subsequently businesses need to respond to policy easing. Failure to do so in the past explains why the PBoC is urging banks to lend more to households and businesses instead of lowering interest rates. After all, Zou Lan, the head of the central bank’s monetary policy department, said on July 13th that there currently is more than enough liquidity in the system.

The post March 2020 economic rebound disappeared almost as fast as it arrived as there was no real improvement in fundamentals. Consumption was still weak, the labour market was uncertain and businesses' investments were low. Today the situation is very similar. Zero covid policies and a collapsing real estate market are not helping. Even China’s export machine could start to wobble if the US, the EU and other developed economies fall into recession later this year. If they do, then policymakers in Beijing will likely accelerate supply-side support measures to keep production high and prices low. Meeting excessively high GDP growth targets would otherwise be difficult for local government officials. Moreover, making sure the manufacturing sector stays competitive has been a key policy goal for Beijing in 2022. With production decelerating amongst competitors in Europe and elsewhere, a growing void is waiting to be filled by state-backed Chinese manufacturers.

About Global Counsel

Global Counsel is a strategic advisory business. We help companies and investors across a wide range of sectors anticipate the ways in which politics, regulation and public policymaking create both risk and opportunity – and to develop and implement strategies to meet these challenges. Our team has experience in politics and policymaking in national governments and international institutions backed with deep regional and local knowledge. Our offices in Brussels, London, Singapore, Washington DC, and Doha are supported by a global network of policymakers, businesses and analysts. Find out morehere.