Insights on China's new policies, reform initiatives and economic data brought to you from Lead Analyst Jens Presthus

6 October 2022

China’s prolonged downturn is revealing where the skeletons are buried

Key takeaways

A growing number of financially “healthy” real estate developers are failing to make debt payments. This has come as a shock to some, even though there have been plenty of warning signs.

There is no evidence to support an imminent turnaround in the sector. President Xi Jinping remains adamant about reducing the size of the sector, despite implications for future growth and the real economy.

This means that entities directly or indirectly tied to the property market will increasingly suffer. Local government defaults are no longer completely unrealistic.

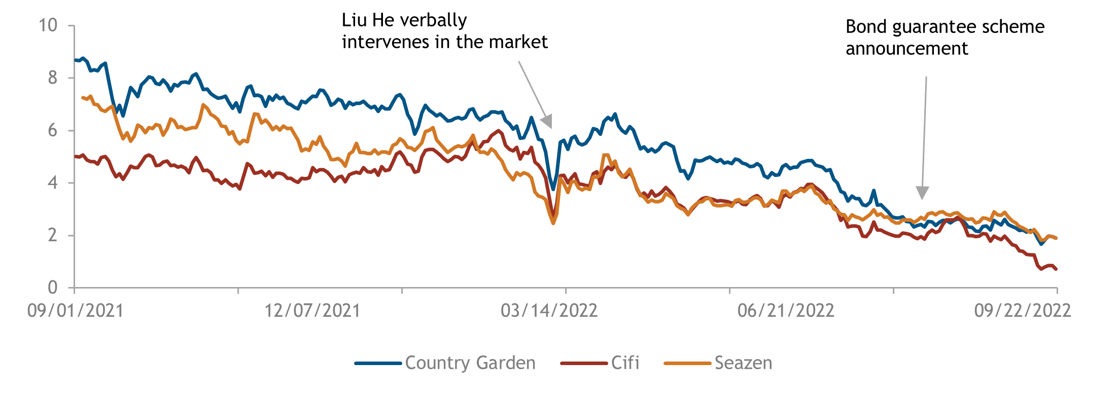

Policy support bounces are usually followed by another leg down

Company share price, HKD

Sources: Investing.com

Not so healthy model developers

Since borrowing restrictions were introduced in August 2020 and Chinese real estate developers started falling into financial distress, the prevailing narrative has been that there are “unhealthy” and “healthy” developers. The idea was simple, some entities – such as Evergrande – were beyond rescue while others would be able to ride out the storm.

This narrative started to show cracks at the beginning of the year when Shimao and Sunac defaulted after failing to make relatively small payments, $101m and $29.5m respectively. In March, Reuters also revealed that Greenland – a major state-backed developer – effectively had been bailed out by the Shanghai authorities in December 2021. Despite all this, the narrative held firm – partly due to widespread belief that the market would stage a turnaround by summer.

There was no turnaround over the summer. Instead, financial stress increased as home sales and prices continued to decline at the same time as banks remained unwilling to offer new financing to developers. To convince banks and investors that it still is safe to lend to property developers on the right side of the three red lines, regulators started promoting a group of “model developers” that they claimed were “healthier” than the rest. After an unsuccessful promotional roadshow, creditors were in August told that the government, through China Bond Insurance, would guarantee new onshore bond issuance by Longfor, Country Garden, Gemdale, CIFI, Seazen and Sino-Ocean.

The scheme has not been a major success, with only a few small issuances. CIFI initially also opted for a private placement targeting friends and family investors – likely because it expected lacklustre public market demand. Many have claimed the slow uptake is due to the good financial health of these developers, that they do not need any external financing. An odd argument given that Country Garden debt for long has been trading at deeply distressed levels and Longfor is struggling to meet its short-term debt obligations – paying its suppliers in flats rather than hard cash. Indeed, data from China Real Estate Information Corporation showed that 2800 real estate entities defaulted on short-term and unsecured “non-standard” debt in August, a 40% increase from the same time last year.

Based on the direction of travel – at both the developer and market level - it should perhaps not have come as a shock that CIFI in late September failed to make a trust product payment. In a surprisingly honest statement, CIFI’s chairman, Lin Zhong, admitted that revenue from projects in Tianjin – one of the country’s worst-performing major cities – was falling short of estimates. Lin said that while the company on paper was sitting on an (unaudited) $4.14 bn cash pile, it was having trouble accessing it partly because funds were held in government-controlled escrow accounts dedicated to project completion. According to Lin, the priority for now is to survive. Chances are chairs of other “model developers” are having the same thoughts.

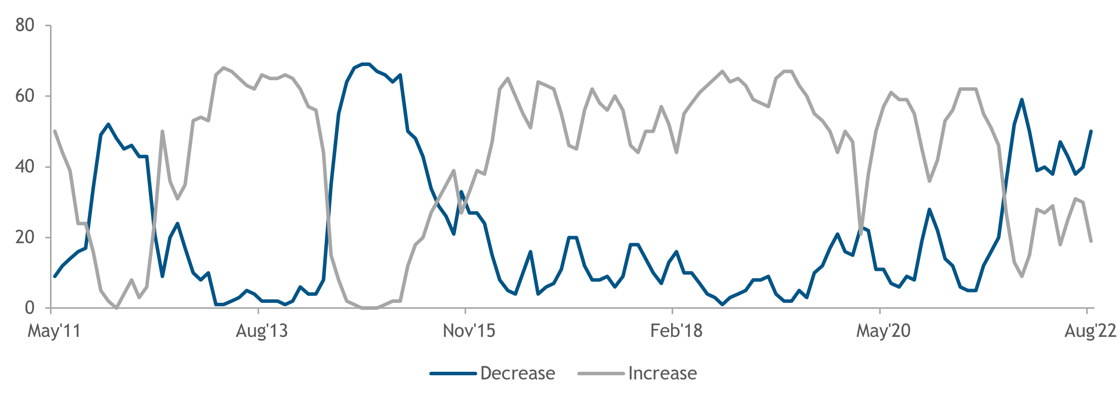

The market is not responding to policy support like during other property downturns

Number of cities with month-on-month home price decrease/increase

Source: NBS

No white knight in sight

The three red lines have now been in place for over two years, with significant implications for the real economy. But Beijing is sticking to its guns even though it is allowing local governments to loosen policy somewhat to avoid a market collapse. It should be clear by now that the property sector will not be revived to its glory days. With a property market in structural decline, a growing number of developers, suppliers and speculators will have to give in. After all, debt payment deadlines cannot be extended forever. Particularly vulnerable are those who rely on revenue from severely distressed local markets, such as CIFI in Tianjin.

More generally, because there is no engine for economic activity that feasibly can replace real estate in the near term, the days of 5-6% annual GDP growth are also over. This means that if your business is a product of the old growth model, chances are you will struggle to survive in this new environment even if you entered the crisis with a healthy balance sheet. It is not by accident that Fosun now is in trouble, fraudulent behaviour at BMW partner Brilliance Auto is coming to the surface and local governments on the brink are selling land to themselves to create “new lines of revenue”.

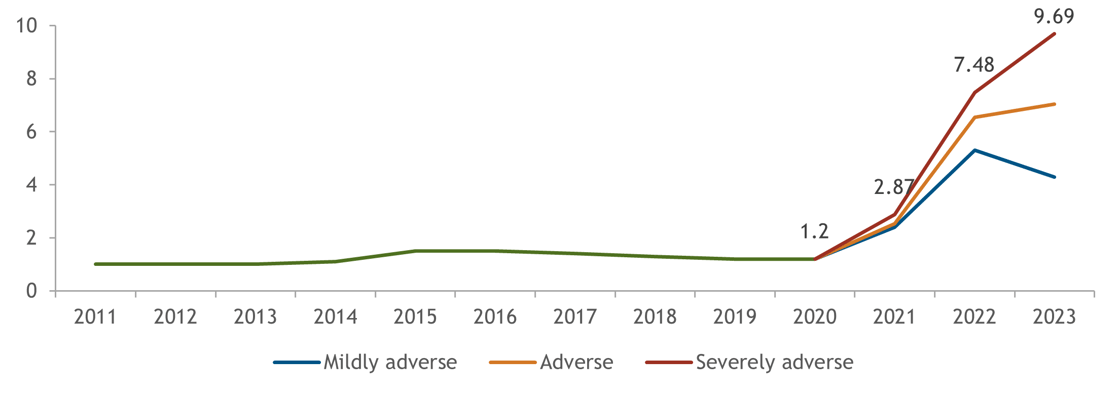

A growing number of forecasters, including the World Bank, are now predicting the Chinese economy to expand by 2.5-3% this year. This would place it in the People’s Bank of China’s “severely adverse” scenario laid out in its 2021 Financial Stability Report. In this scenario, the central bank expects the NPL ratio at 30 large banks to jump from 2.9% in 2021 to 7.5% in 2022 - a number that would be significantly higher if the scenario included rural banks with less power vis-à-vis local governments and therefore also lower lending standards. Indeed, a number of small rural banks have already gone bust.

Bad debt is rising fast throughout the banking system

NPL ratio at 30 large banks in PBoC stress test scenarios, severely adverse = GDP growth at 2.8% in 2022 and 2.1% in 2023

Source: PBoC

What has become clear is that very few people understand the financing structures that have allowed Chinese companies, including real estate firms, to grow so fast for so long. And because of this, very few people (if any) understand how a structural and economy-wide slowdown will impact their balance sheets. What the last two years have illustrated, however, is that such a slowdown will reveal where the skeletons are buried.

About Global Counsel

Global Counsel is a strategic advisory business. We help companies and investors across a wide range of sectors anticipate the ways in which politics, regulation and public policymaking create both risk and opportunity – and to develop and implement strategies to meet these challenges. Our team has experience in politics and policymaking in national governments and international institutions backed with deep regional and local knowledge. Our offices in Brussels, London, Singapore, Washington DC, and Doha are supported by a global network of policymakers, businesses and analysts. Find out morehere.