Insights on China's new policies, reform initiatives and economic data brought to you from Lead Analyst Jens Presthus

15 December 2021

Rebalancing on hold as Beijing returns to its old playbook

The Central Economic Work Conference, which concluded on December 10th, confirmed what had become a poorly kept secret. The Chinese leadership sees trouble ahead and is willing to pause its debt reduction efforts to maintain social stability ahead of the 20th Party Congress in late 2022. Fiscal spending will increase and restrictions on the property sector will ease. To ensure stability, expect increased support for SOEs and an even more prominent role for the state in the economy.

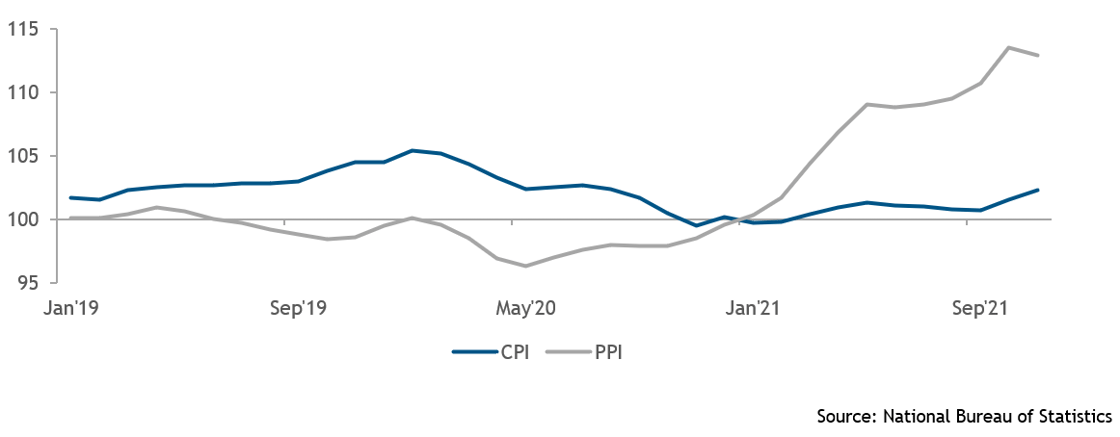

Inflationary pressures are returning to Chinese households

Consumer and producer price indexes, previous year = 100

Key takeaways

Social stability, job creation and 5-6% GDP growth are the main policy priorities for 2022. This means a return to infrastructure investment and rising debt levels.

Big-ticket reforms are being planned, but Beijing is still counting on the rest of the world to achieve its policy goals in the coming year. The US will likely have to absorb China’s domestic demand deficiencies, which could re-ignite trade tensions.

The property sector will likely see restrictions eased, but SOEs will benefit the most. Private sector monopolies should also expect continued scrutiny, as Beijing seeks to guide “barbaric” capital towards its own development plans.

Stability was the word of the day

The leadership meeting emphasised three main headwinds for economic growth in 2022: demand contraction, weakening expectations and supply shock. The first two are directly linked and point to the fading consumption rebound that supported growth in 2021. And while China might have managed to escape most of the negative health effects of the pandemic, its economy is suffering from semiconductor shortages and high energy prices. The third headwind will be difficult for the government to solve in the short term, but policymakers promised to deal with the former two and keep economic growth in a “stable range”. Because 2022 will be a politically sensitive year, with President Xi Jinping to commence his third term in office, economic stimulus will be increased to support job creation and social stability.

Prioritising supply over demand

Immediate support for households is missing, but steps are being taken to increase consumption and reduce savings over the long term. Despite awareness about weakening consumer confidence, slowing wage growth and creeping inflation that Chinese consumers so far have been shielded from, few details were revealed about how Beijing intends to not only support, but also increase domestic demand in 2022. Tax and fee cuts were mentioned, but this has become standard procedure and the policies do not seem to have much effect. However, policymakers did stress that they are looking at ways to remove the Hukou, or urban registration system, for most cities. There is now a growing understanding that access to public services need to be tied to where people live rather than where they are registered citizens. If implemented properly, this would give millions of migrant workers access to public education and healthcare, and therefore reduce the need for them to save an outsized share of their income.

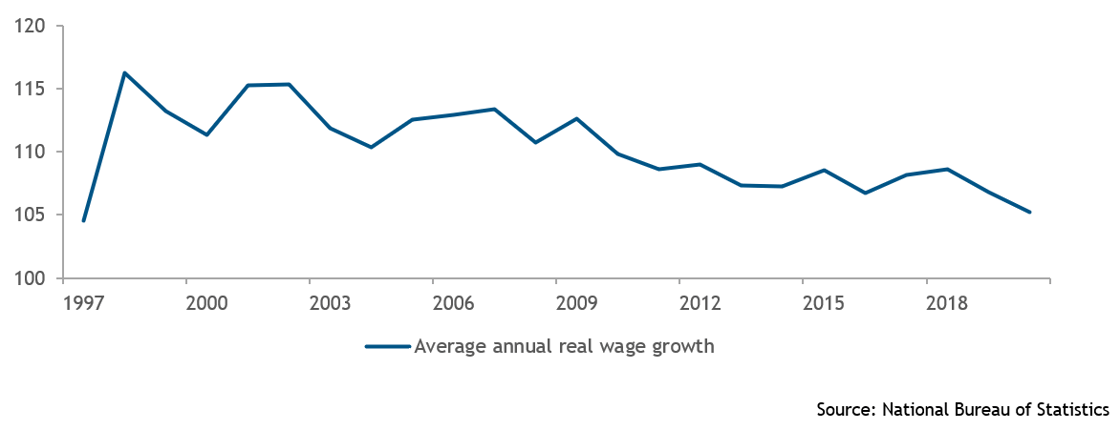

Wage growth has slowed since the financial crisis, and tumbled since 2018

Average annual real wage growth index, previous year = 100

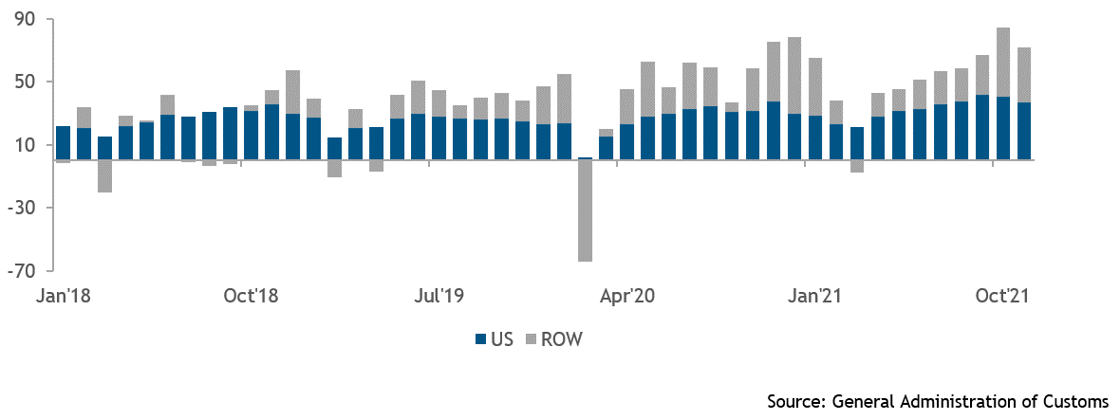

Beijing has decided to return to its old playbook and boost the supply side. The Chinese leadership seems unwilling to accept economic growth below 5-6%. But it is also aware that it will take years for consumption-stimulating policies to take effect, and that it therefore is necessary in the short-term to return to its old strategy of accelerating infrastructure investment and increasing support for the manufacturing sector. And because the former in large part will take the form of investment in non-productive transportation infrastructure, local government debt is likely to resume its rise after a short pause in 2021. While this should be supportive for commodity producers – both Chinese and foreign – it also means that the rest of the world, most notably the US, will have to continue to support Chinese growth by absorbing its excess supply, or domestic demand deficiencies. And with the US trade deficit with China remaining a contentious issue under President Joe Biden, it is not unlikely that trade tensions will increase again in the new year.

The US continues to absorb an outsized share of Chinese exports

Trade balance with the US and ROW, in $ bn

It was highlighted that monetary policy should remain stable and moderate, meaning significant policy support should not be expected from the central bank. Although the political elite in Beijing might want the People’s Bank of China (PBoC) to offer more support, they are both aware of the limited impact further easing will have on the real economy. China’s problem, akin to the US, EU and Japan, is not that there is too little liquidity, but rather that it is not flowing where it is supposed to. Stable SOEs are being favoured over cash-strapped and risky SMEs, and because weak business confidence is depressing borrowing for investment purposes, too much liquidity is finding its way into financial markets – building up volatility that China’s regulators want to avoid. Policymakers said during the meeting that they want to guide financial institutions to support the real economy, but unless banks are explicitly told to change their funding priorities, it will be hard for looser monetary policy to make a real impact.

Respite for (state) developers, but not for monopolies

Officials warning against policies that can have a “contracting effect” on the economy signal that the real estate market may get a regulatory respite in 2022. Because of its importance to the overall economy, further easing should be expected for the property sector. Engineering a sharp and lasting downturn, which arguably is needed to deal with the excesses of the market, is not fitting for a politically sensitive 2022 that is all about stability. However, supportive policies will mostly be targeted at “favoured” entities. A whitelist that was issued to state banks by the PBoC in mid-November laid out which public and private developers should receive preferential treatment and access to funding. It also described plans for consolidating the state’s position in the industry, building on recent comments by President Xi Jinping about strengthening the position of SOEs. This aligns well with the government’s focus on increasing supply of public housing and means that profit-hungry private developers likely will see their operating environment remain challenging.

Tough language on market abuse and the negative effects of “barbaric” capital underscore that anti-monopoly efforts will remain a key priority. While “boosting market confidence” was highlighted as an important goal, it was also stressed that anti-monopoly work needed to be strengthened. Vague plans for a new “traffic light” system was announced, to prevent “barbaric expansion of capital”, and to help guide private capital to where it will support the government’s own development plans. These are hardly announcements that signal that large internet platforms will have an easier time ahead. Indeed, while large-scale layoffs, as a consequence of the regulatory campaign, have been unpopular in Beijing, it also seems like that is a price the leadership is willing to pay. “Boosting market confidence” therefore seems to be targeted at SMEs and young entrepreneurs, probably because it is easier to guide and shape their strategic priorities and long-term development plans.

About Global Counsel

Global Counsel is a strategic advisory business. We help companies and investors across a wide range of sectors anticipate the ways in which politics, regulation and public policymaking create both risk and opportunity – and to develop and implement strategies to meet these challenges. Our team has experience in politics and policymaking in national governments and international institutions backed with deep regional and local knowledge. Our offices in Brussels, London, Singapore, Washington DC, and Doha are supported by a global network of policymakers, businesses and analysts. Find out morehere.