Insights on China's new policies, reform initiatives and economic data brought to you from Lead Analyst Jens Presthus

16 February 2023

RMB internationalisation: 12 months after America weaponised the dollar

Key takeaways

Unprecedented weaponisation of the dollar following Russia’s invasion of Ukraine has not kickstarted a shift away from the USD to an alternative currency, such as the RMB.

To the contrary, the RMB has become less popular since the start of the war in Ukraine, partly because of increased Taiwan-related risk.

China and a small group of “like-minded” countries have started discussions about creating a new alternative currency. This is easier said than done, with few prospects for success.

The RMB is becoming less, not more attractive

18 months ago I wrote a blog arguing that domestic political, financial and economic conditions are more important to RMB internationalisation than shifts in the geopolitical environment. In short, as long as China needs to keep its capital account relatively closed to protect its fragile financial system, and as long as Beijing adheres to an export-oriented economic model that depends on a weak currency, the RMB will never become a widely used global currency that can challenge the USD. This argument still holds true. Indeed, as capital inflows in 2020 and 2021 turned into rapid outflows in 2022, the People’s Bank of China quickly started tightening capital controls.

It has also become evident over the last 12 months that increased geopolitical tension between world powers, including the US, China and Russia, which is often used as an argument for de-dollarisation, has had the opposite effect. Even with unprecedented weaponisation of the dollar after Russia’s invasion of Ukraine, the RMB has become less attractive relative to the USD.

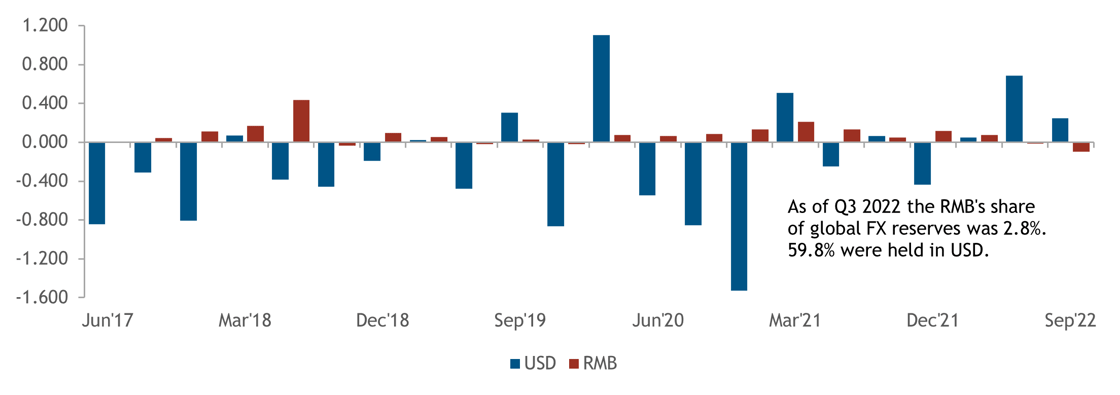

Dollar-assets are increasing in popularity despite weaponisation of the USD

Quarterly ppt change in global FX reserves held as USD and RMB

Source: IMF

The RMB’s share of global FX reserves has increased more or less every quarter since the IMF started tracking it in 2017. Conversely, the USD share has been steadily declining. This trend was flipped on its head after Russia invaded Ukraine - going against the narrative that harsh financial sanctions would accelerate a shift away from the dollar. This can partly be explained by the dollar’s traditional safe haven role, and the relative attractiveness of US Treasuries as the Federal Reserve consistently hiked rates throughout 2022. But it is also likely that Russia’s invasion of Ukraine, and Beijing’s backing of Moscow, have pushed up the RMB’s geopolitical risk premium.

Indeed, for an increasing number of corporates and investors, Taiwan-risk has become a real consideration. No one wants to end up in another “Russia-style” scenario in which US sanctions create billions of dollars in stranded assets. Although most institutional investors will keep their public market exposure to China, they are rapidly scaling down investments in private markets. It is telling that Singapore’s GIC, which has been one of the biggest proponents of the “China growth story”, and which arguably knows China better than most, is saying political and geopolitical risk is prompting it to scale down exposure.

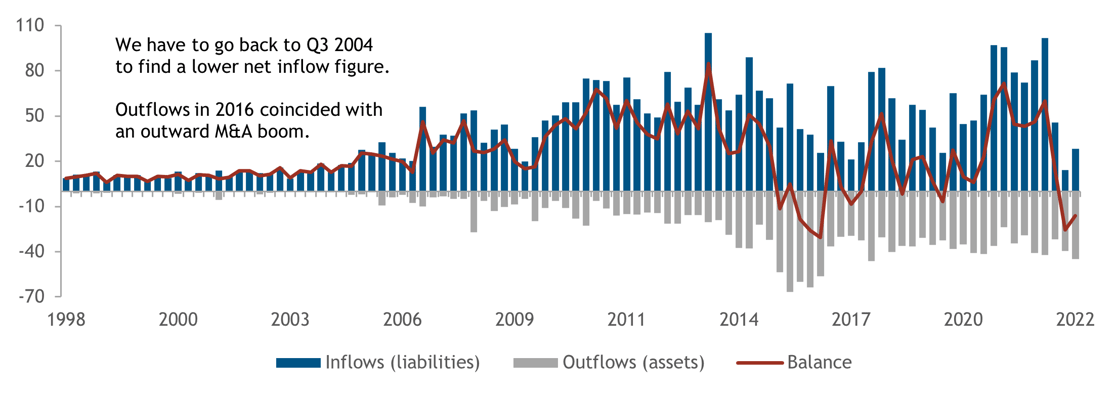

Foreigners are rethinking their private market exposure to China

Quarterly direct investment flows, $ bn

Source: State Administration of Foreign Exchange

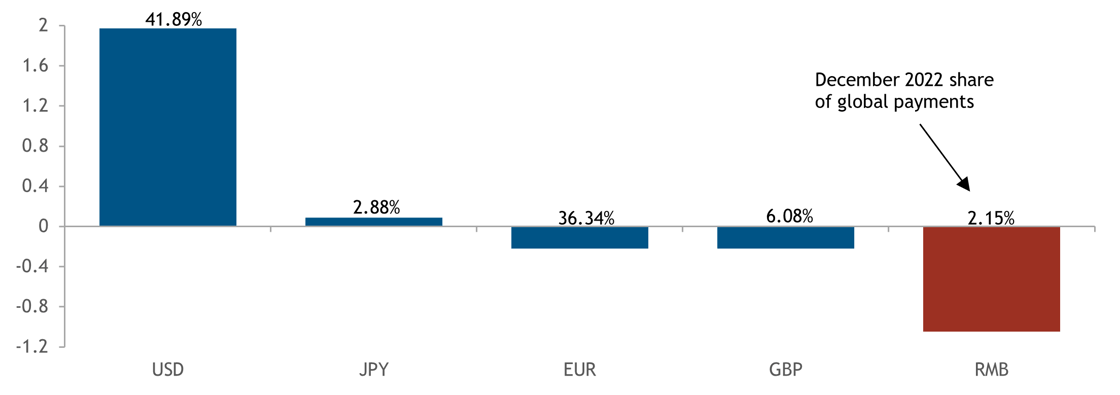

The same pattern can be seen in the currency composition of global payments. After steadily increasing and peaking at 3.2% in January 2022, the RMB’s share dropped to 2.23% the month after and has barely moved since. The USD, on the other hand, saw its share increase from 39.9% to 41.9% between January and December 2022. Although it should be noted that the RMB’s share in trade finance has increased since the start of the war, from 1.9% in January 2022 to 3.9% in December the same year, it is still way down from its peak of around 9% almost a decade ago - at which time the RMB was the second most used currency in trade finance.

The dollar is staging a global payments comeback, at the expense of the RMB

Jan-Dec 2022 ppt change in share of global payments by top 5 currencies

Source: SWIFT

While these numbers may start to increase again should China follow through on plans to settle more bilateral trade in RMB, the significance should not be overstated. For the countries that China is pursuing such agreements with, including Saudi Arabia and Indonesia, it does not matter much if they receive RMB or USD in payment for their China-bound exports. Most of this income will be recycled into imports from China anyways. What matters is if these countries start to recycle their trade surpluses into RMB-denominated reserve assets.

China’s clique of like-minded countries has few alternatives to the dollar

Making the RMB an attractive alternative to the USD has long been an aspiration in Beijing. But it was only after the US in 2022 showed a real willingness to weaponise the dollar that policymakers and regulators properly started paying attention to the wider issue of making China less exposed to the dollar-based global economy. Following an emergency meeting in April 2022 between regulators and domestic and foreign banks on how to protect overseas Chinese assets against US sanctions, Beijing has had similar discussions with “like-minded” countries. The idea of a BRICS currency was floated during the group’s summit in 2022, and the Russians have said the issue will be a topic of discussion when the group meets in South Africa in August. Iranian participation may also have been debated when the country’s president, Ebrahim Raisi, and his new central bank governor, Mohamed Reza Farzin, arrived in Beijing for talks with President Xi Jinping on February 14th.

The problem, however, is there are only a small group of countries that have any real interest in creating such an alternative reserve currency regime. And as GAM’s Paul McNamara explains in his recent FT piece, positing it is not a particularly straightforward process.

This crystallises the point about how there currently are no feasible alternatives to the dollar as the world’s reserve currency – a peculiar problem for the surplus countries who desperately want to reduce their exposure to it. Besides investment in raw materials or strategic infrastructure in BRICS-like countries, China has few options but to park its trade surplus in dollar assets. The same is true for Beijing’s BRICS partners (especially India) and commodity-rich nations in the Gulf, who remain sceptical about accumulating large amounts of RMB-denominated reserves. Indeed, while there clearly are risks linked to holding dollar assets, for most countries they are unlikely to be larger than the geopolitical and domestic risks associated with holding Chinese assets.

About Global Counsel

Global Counsel is a strategic advisory business. We help companies and investors across a wide range of sectors anticipate the ways in which politics, regulation and public policymaking create both risk and opportunity – and to develop and implement strategies to meet these challenges. Our team has experience in politics and policymaking in national governments and international institutions backed with deep regional and local knowledge. Our offices in Brussels, London, Singapore, Washington DC, and Doha are supported by a global network of policymakers, businesses and analysts. Find out morehere.